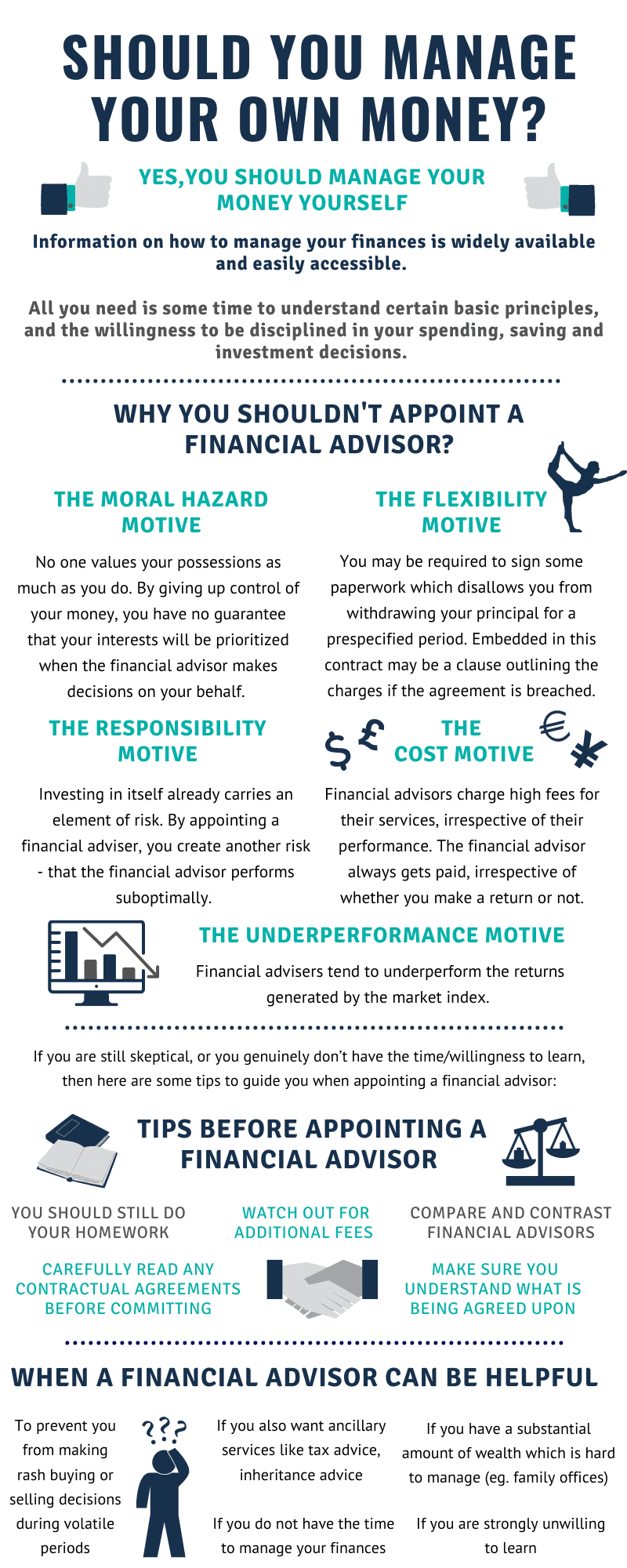

There are several distinct benefits to using a fee only financial planner. These advisors will be more independent and act as fiduciaries. While fee-only advisors may charge by the hour, retainer, percentage of assets under management (AUM), or flat fee, you must be aware of any conflicts of interest and ask about them. Fee-only financial advisors might not be the right fit for all. For example, some fee-only financial planners may not be appropriate for people with high-incomes, whereas others may be best suited to clients with more modest incomes.

Fee-only financial advisors are less likely to be independent.

Non-fee-only financial advisors are more likely to be self-employed than their fee-only counterparts. These planners get paid by clients directly, either by flat fees or by a percentage. This means that they do not earn commissions on the financial products they suggest and have no conflicts of interests. They are more likely to be experts in many areas.

Consult a directory for financial advisors to help you find a fee-only, qualified financial planner. The Financial Planning Association offers a searchable directory of advisors in your area. Once you've done this, you can filter the results by fee-only financial planners and determine whether the advisor is independent. It is shown in the profiles of advisors that they have been compensated. The services an advisor offers will determine whether or not they are independent.

They act as fiduciaries

A fiduciary is someone who charges money to advise you on how to invest your money. This means that they are legally required to act in your best interest, and disclose any impropriety. Both registered financial advisors and certified financial planning professionals are considered fiduciaries. There is a significant difference between these types of financial advisors. These are some of the main differences between financial advisors.

A fee only planner may not have as much knowledge about all topics. They may not not be able assist with everything, such as estate planning. A fee-only planner on the other side can help you to identify problems such as taxes or probate and work towards your objectives. He or she may also provide feedback on how you are doing. Some people may find fee-only financial planning a good fit.

They can charge hourly, retainer (percentage of assets), flat fee, or hourly

Fee-only financial planning offers many benefits. One of them is the simplicity of the fee structure. Planners are able to reach non-accountable clients through this structure. It is also flexible because the hourly fee does not correlate with income or AUM. The financial situation of clients will determine the AUM fee.

There are some notable benefits to fee only financial planning. However, there are also significant drawbacks. For example, clients may not know what the planning process will involve. They also have little control over the cost because the planner decides what is fair. Planners may feel compelled to spend more time on planning if they charge high fees, or to be less proactive.

They have to justify conflicts of interest

Conflicts of interest and fee only financial planning are two sides of the same coin in the financial industry. In the former case, the financial advisor acts in the client's best interest and is bound by fiduciary standards. The latter situation, however, is where the financial planner receives compensation only through client fees. The conflict of interest the financial planner has must be disclosed to clients. Financial planners should never be paid referral fees and commissions.

Conflicts of Interest are inevitable no matter what model financial advisors follow. There are many conflicts. Some conflicts can be managed and are in line with the fiduciary standard, while others cannot. Clients should be made aware of any conflicts of interests so they are able to trust financial advice from their advisor. These are some helpful tips for managing conflicts.

FAQ

What is retirement plan?

Financial planning includes retirement planning. It allows you to plan for your future and ensures that you can live comfortably in retirement.

Retirement planning involves looking at different options available to you, such as saving money for retirement, investing in stocks and bonds, using life insurance, and taking advantage of tax-advantaged accounts.

What is risk-management in investment management?

Risk management is the act of assessing and mitigating potential losses. It involves monitoring, analyzing, and controlling the risks.

Risk management is an integral part of any investment strategy. Risk management has two goals: to minimize the risk of losing investments and maximize the return.

The following are key elements to risk management:

-

Identifying the risk factors

-

Monitoring the risk and measuring it

-

How to control the risk

-

How to manage the risk

What is estate planning?

Estate Planning refers to the preparation for death through creating an estate plan. This plan includes documents such wills trusts powers of attorney, powers of attorney and health care directives. These documents will ensure that your assets are managed after your death.

Who should use a Wealth Manager

Anyone looking to build wealth should be able to recognize the risks.

It is possible that people who are unfamiliar with investing may not fully understand the concept risk. Poor investment decisions could result in them losing their money.

The same goes for people who are already wealthy. They might feel like they've got enough money to last them a lifetime. But this isn't always true, and they could lose everything if they aren't careful.

Everyone must take into account their individual circumstances before making a decision about whether to hire a wealth manager.

How do I get started with Wealth Management?

It is important to choose the type of Wealth Management service that you desire before you can get started. There are many Wealth Management options, but most people fall in one of three categories.

-

Investment Advisory Services: These professionals can help you decide how much and where you should invest it. They can help you with asset allocation, portfolio building, and other investment strategies.

-

Financial Planning Services – This professional will help you create a financial plan that takes into account your personal goals, objectives, as well as your personal situation. Based on their professional experience and expertise, they might recommend certain investments.

-

Estate Planning Services- An experienced lawyer will help you determine the best way for you and your loved to avoid potential problems after your death.

-

Ensure they are registered with FINRA (Financial Industry Regulatory Authority) before you hire a professional. Find someone who is comfortable working alongside them if you don't feel like it.

Statistics

- As of 2020, it is estimated that the wealth management industry had an AUM of upwards of $112 trillion globally. (investopedia.com)

- These rates generally reside somewhere around 1% of AUM annually, though rates usually drop as you invest more with the firm. (yahoo.com)

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

External Links

How To

How to Invest Your Savings To Make More Money

You can make a profit by investing your savings in various investments, including stock market, mutual funds bonds, bonds and real estate. This is called investing. It is important to understand that investing does not guarantee a profit but rather increases the chances of earning profits. There are many ways you can invest your savings. Some of them include buying stocks, Mutual Funds, Gold, Commodities, Real Estate, Bonds, Stocks, and ETFs (Exchange Traded Funds). These methods are described below:

Stock Market

The stock market allows you to buy shares from companies whose products and/or services you would not otherwise purchase. This is one of most popular ways to save money. Buying stocks also offers diversification which helps protect against financial loss. If the price of oil falls dramatically, your shares can be sold and bought shares in another company.

Mutual Fund

A mutual fund can be described as a pool of money that is invested in securities by many individuals or institutions. They are professionally managed pools with equity, debt or hybrid securities. The mutual fund's investment objective is usually decided by its board.

Gold

It has been proven to hold its value for long periods of time and can be used as a safety haven in times of economic uncertainty. Some countries use it as their currency. Due to the increased demand from investors for protection against inflation, gold prices rose significantly over the past few years. The price of gold tends to rise and fall based on supply and demand fundamentals.

Real Estate

Real estate includes land and buildings. If you buy real property, you are the owner of the property as well as all rights. Rent out a portion your house to make additional income. You may use the home as collateral for loans. You may even use the home to secure tax benefits. You must take into account the following factors when buying any type of real property: condition, age and size.

Commodity

Commodities include raw materials like grains, metals, and agricultural commodities. Commodity-related investments will increase in value as these commodities rise in price. Investors who want the opportunity to profit from this trend should learn how to analyze charts, graphs, identify trends, determine the best entry points for their portfolios, and to interpret charts and graphs.

Bonds

BONDS can be used to make loans to corporations or governments. A bond can be described as a loan where one or both of the parties agrees to repay the principal at a particular date in return for interest payments. Bond prices move up when interest rates go down and vice versa. An investor purchases a bond to earn income while the borrower pays back the principal.

Stocks

STOCKS INVOLVE SHARES of ownership within a corporation. Shares represent a fractional portion of ownership in a business. You are a shareholder if you own 100 shares in XYZ Corp. and have the right to vote on any matters affecting the company. You also receive dividends when the company earns profits. Dividends are cash distributions paid out to shareholders.

ETFs

An Exchange Traded Fund (ETF), is a security which tracks an index of stocks or bonds, currencies, commodities or other asset classes. Unlike traditional mutual funds, ETFs trade like stocks on public exchanges. The iShares Core S&P 500 (NYSEARCA - SPY) ETF is designed to track performance of Standard & Poor’s 500 Index. This means that if you bought shares of SPY, your portfolio would automatically reflect the performance of the S&P 500.

Venture Capital

Venture capital is private funding that venture capitalists provide to entrepreneurs in order to help them start new companies. Venture capitalists can provide funding for startups that have very little revenue or are at risk of going bankrupt. Usually, they invest in early-stage companies, such as those just starting out.